![Avoiding the Potholes [and Pitfalls] with Last-Mile Delivery](assets/images-t1768511628/15021.webp)

Because of the current pandemic, it should come as no surprise that online shopping for the current holiday season has exceeded all previous records. Recent consumer data revealed that 71% of U.S. adults plan to do more than half of their holiday shopping online. Many retailers are also providing free shipping to increase sales. While FedEx, UPS, and Amazon may make most of the deliveries, many commercial motor carriers providing last-mile delivery can also expect an increase in miles driven and deliveries made.

Motor carriers are familiar with the possibility of catastrophic accidents. (HeplerBroom's Rapid Response Team provides emergency on-site services when such an event occurs.) With last-mile deliveries, however, other types of claims can be expected. For example, driving a big rig in a local neighborhood can lead to fender benders or damage to a homeowner's property. Because drivers performing last-mile deliveries are also installing products such as appliances and other durable goods, defective installations may lead to personal injury claims. Those same drivers may also sustain work-related injuries not otherwise common to truck drivers.

The article[i] below (which co-author Kelley Millaway and I previously published in an edition of the Trucking Industry Defense Association’s newsletter) provides a more detailed discussion of the potential exposures and possible protections available to carriers.

* * * * *

The expansion of e-commerce and use of online shopping has led to significant development within the market for last-mile delivery. Additionally, with consumers shopping online for larger items, such as appliances, merchants have shifted away from the use of carriers such as FedEx and UPS that carry mostly smaller items, and have started using carriers that can provide last-mile services that consumers have come to expect, such as tracking options and scheduled deliveries.

Several trucking companies have noticed this change in the last-mile market and have expanded their operations to provide delivery services consumers and merchants are seeking. Many companies have found a niche market and have even started offering assembly and installation along with delivering products to consumers.

A[n] article published by Bloomberg examined the types of services trucking companies are providing in their last-mile deliveries. Numerous companies referenced in the Bloomberg article now have their drivers deliver kitchen appliances and furniture—to name a couple of products—as well as unpack, assemble and install such products at purchasers’ homes. J.B. Hunt uses both third-party contractors as well as its own drivers to carry out these tasks. As employees take on more responsibility, there is a greater chance employees will commit negligent acts in the course of delivering and installing products.

However, with the expansion of traditional cartage services comes an increased risk of liability. Trucking companies need to be aware of the potential claims they face in providing these new services, and what protections they have against such claims, as they travel the last mile to their destination.

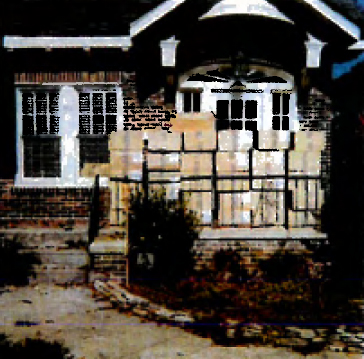

[In 2019], Spanx Founder and CEO Sara Blakely posted on LinkedIn this photo of the front porch of her apartment that served as Spanx Headquarters in the early days of Spanx.

The carrier’s act of leaving the boxes as it did arguably created a hazardous condition and the potential for liability. With ingress and egress blocked, imagine if the occupant was trapped inside and a fire broke out. The owner or occupant might sue the carrier under various theories of negligence. Premises liability claims are likely. Product liability claims may be pursued. The typical negligent supervision, training, hiring and retention claims brought against trucking companies may take on more traditional tort claims based on a driver’s conduct and vicarious liability.

Another issue for trucking companies to consider is whether liability insurance would apply to such claims. Trucking companies typically obtain liability insurance under commercial auto policies, which generally provide liability coverage only for those claims that arise from the ownership, maintenance or use of a covered motor vehicle. Claims that arise out of the negligence of a driver in delivering or installing a product may not be considered to arise out of the ownership, maintenance or use of a covered auto, and insurance companies are likely going to deny coverage under commercial auto policies.

Another option for insurance coverage for these claims may exist through commercial general liability (“CGL”) policies. Such policies provide coverage for claims of bodily injury or property damage that arise out of an “occurrence” or accident. As demonstrated above, trucking companies can face claims of bodily injury resulting from negligently delivered products; however, trucking companies may also face claims of bodily injury resulting from negligently installed products. An improperly installed kitchen appliance or an improperly assembled item of furniture may result in bodily injury to an individual, thereby exposing the trucking company to another type of claim for bodily injury. The same holds true for claims of property damage.

A trucking company venturing into these last-mile services should be aware that the amount of coverage provided by a CGL policy is likely very limited. CGL policies contain several exclusions that may apply. The “Expected or Intended Injury” exclusion in such policies removes coverage if the insured reasonably could have expected or intended the property damage or the claimant’s injury, even if it was of a different degree or type than actually expected or intended. For example, if a claimant alleges that a driver was not adequately trained in delivery or installation, an insurance company may argue that the trucking company could have expected the claimant’s injury and raise this exclusion as a defense to coverage.

Another potential exclusion could be for “Damage to Property and Damage to Your Product” which removed coverage, in relevant part, for property damage to that particular part of any property that must be restored, repaired or replaced because the insured’s work was incorrectly performed on it. This portion of the exclusion applies only to property damage to the product that is being delivered and/or installed. Thus, an insurance company can raise this exclusion as a defense to coverage for claims of property damage that involves damage to the delivered or installed product that must be restored, repaired or replaced because a driver incorrectly delivered or installed it.

The Damage to Your Product exclusion precludes coverage for property damage to a product that is manufactured, sold, handled, distributed or disposed of by the trucking company. Because trucking companies at least “handle” the delivered or installed products, insurance companies will likely raise this exclusion as a coverage defense for claims of property damage to products that are delivered or installed by trucking companies.

Finally, CGL policies typically contain “Employer’s Liability” exclusions, which remove coverage for claims of bodily injury to an employee if the employee’s injury arises out of the performance of their duties related to the conduct of the insured’s business. If a driver were to sustain an injury while delivering or installing a product, such injury likely will be considered to arise out of their duties related to the trucking company’s business of delivering and installing products. However, the reason this exclusion exists in CGL policies is because such claims would be covered by a workers’ compensation policy. Will a Worker’s Compensation Policy cover activities beyond driving, loading and unloading?

Trucking companies are not without options. For instance, if trucking companies are contracting with manufacturers to deliver and install their products, they may negotiate with the manufacturer to require the manufacturer to obtain liability insurance which names the trucking company as an additional insured. Additionally, trucking companies should investigate whether an endorsement may be added to a CGL policy which would cover claims of bodily injury or property damage arising out of a product that is delivered or installed by the trucking company.

Before trucking companies make the decision to expand their services to include last-mile deliveries, they must consider the level of risk exposure associated with this type of service. Adding last-mile delivery to a trucking company’s offered services exposes trucking companies to additional bodily injury and property damage claims. As the holidays approach, there are likely to be more deliveries like those made to Ms. Blakely’s apartment. Thus, trucking companies should stay informed of the potential liability they face and take the appropriate steps to ensure they are minimizing risk and maximizing coverage for any potential claims. Otherwise, the last-mile delivery may be a trucking company’s first mile to the courthouse.

[i] “Avoiding the Potholes {and Pitfalls} with Last-Mile Delivery,” TIDA Newsletter (Fall 2019). Reprinted with permission.

Partner

PartnerAs the head of HeplerBroom’s 24-hour Emergency Response Team, Michael Reda knows what it takes to defend commercial trucking companies and their drivers. His calm presence helps diffuse the adrenaline that can be present at ...

{kind=link}